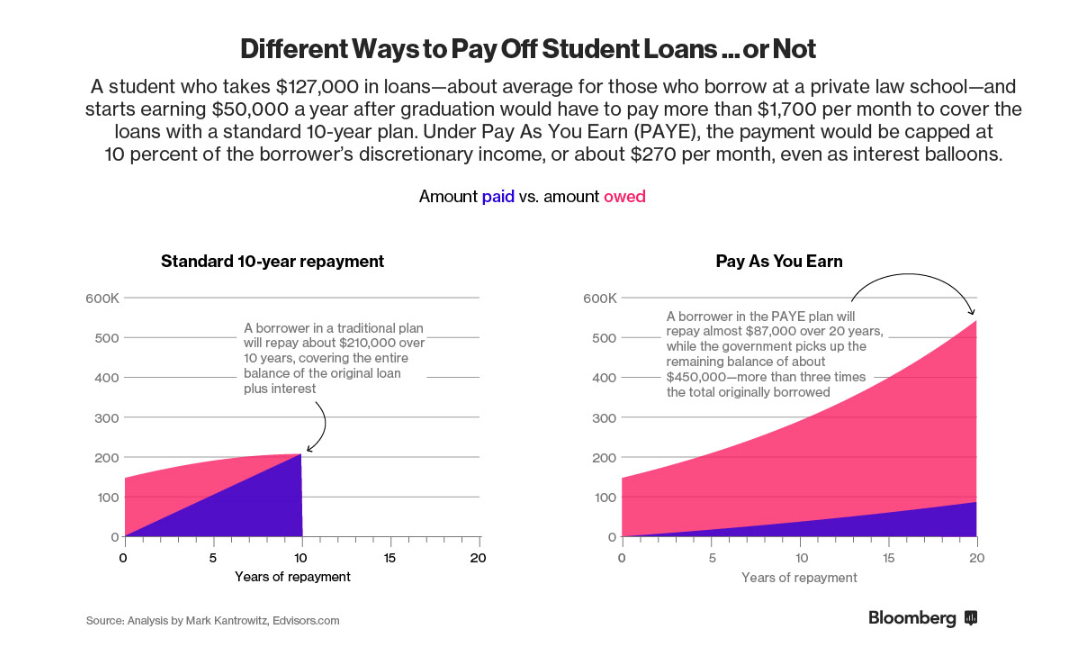

Here’s how to borrow $127,000 in student loans, only repay $87,000 over twenty years, and have the U.S. Government pick up the tab for the $450,000 still owed at the end of the repayment period. [Notice the quadrupling effect on the total balance owed because of the interest that accrues in the two decade long repayment period? ]

- Go to Law School

- Borrow the 2015 average amount of Federally guaranteed graduate student loans, or $127,000

- Qualify for the Pay As You Earn (PAYE) repayment plan—a special plan where a borrower owes as little as 10% of discretionary income or $270 per month, versus the Standard Plan where a student would owe $1397.00 per month for 10 years.

- Make regular $270 per month payments for 20 years, while the interest grows. BTW, economic hardship deferments of up to 3 years within the 20 years also count within the repayment period. Basically, 17 years of actual payments will satisfy the requirements for loan forgiveness.

- The U.S. Government will “forgive” the remaining balance, which includes two decades of daily compounding interest, or $450,000.

Borrower beware: while having the $450,000 balance forgiven is quite a subsidy, borrowers may have to pay income tax on the amount forgiven. At the average American tax rate of 10.1%, borrowers may owe $45,450 in the year their loans are forgiven. In addition, think about the costs of basically breaking a promise to the government by defaulting on loans given in good faith, in terms of weighing on your conscience.

U.S. Taxpayers beware: Currently, $200 Billion of the $1.2 Trillion student debt is being repaid under an income based repayment plan. For the student loans added in 2015 and beyond, U.S. taxpayers are forecasted to shoulder an additional $39 billion in costs.

Income based repayment plans offer borrowers flexibility in repaying debt. Yet, the costs include two decades of repayments, and the knowledge that others are going to involuntarily assume the bulk of one’s financial obligations. And, as each year the average amount of student debt continues increasing, while the job outlook continues to remain challenged, income based repayment may become the repayment plan of choice. The newest generation of adults may be handicapped with their own personal student debt and the responsibility of repaying other’s student debts, not to mention the national debt accrued by previous generations.

For more information, see Bloomberg News